“Joe Strummer” is the pseudonym of a frequent commenter on BloodhoundBlog. He runs a weblog of his own — under a different pseudonym — and leads a life of joy, contemplation and undisturbed privacy under his real name. But no matter how he is denominated, Strummer is an expert in the Austrian School of Economics, a colloquium of great minds who are, alas, the eternally unheeded Cassandras of the decline of Western Capitalism. In this essay, penned yesterday, Strummer shares with us his reflections upon the burgeoning economic crisis:

My thoughts on the looming crisis

by Joe Strummer

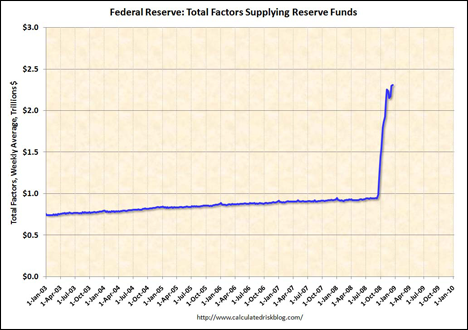

This is a graph of the nominal value of the assets that the Fed has “owned” over time. Notice the fairly flat, slightly rising line until September/October of 2008.

Two points about this graph. First, the Fed did not get value for the $1.2 trillion it has purchased in “assets” since October. The $1.2 trillion in nominal value is actually nearly worthless. That’s because these “assets” are the mortgage backed securities backed by now- or soon-to-be-broken promises to pay by individual homeowners.

Second, the Fed has merely pumped about 1.2 trillion of dollars into the market place free. In other words, it has taken nothing out of the economy of value. When the government adds currency – what Jim Cramer calls, dropping wads of cash from helicopters – without getting anything in return, it’s called inflation.

Now, $1.2 trillion in new currency is bad, but not nearly as bad as when the Fed loans money to banks at a .5 interest rate. The Fed simply is printing money for any bank that wants to borrow it at .5 percent. Consequently, banks are now borrowing to 1) cover the losses they incurred to make themselves solvent, and 2) to have cash reserves that they can then use when the economy picks up to lend at future, higher interest rates.

All of this inflation hasn’t hit the real economy because banks are hoarding that money to wait for better borrowers or because borrowers simply are hunkered down right now trying to wait out the storm.

When the economy starts to improve a bit, and borrowers start coming out of the woodwork to borrow money for homes, or to build or expand businesses, banks are going to start lending again. And when they do, every bank will have a ton of cash to lend. That excess in currency is the inflation that will very rapidly hit the real economy as each bank seeks to push more and more of its cash into the economy. The inflationary-lending cycle will feed on itself.

At the first sign of inflation, the Fed is going to clamp down. Inflation is harmful because it erodes the real wages & purchasing power in the economy. People on fixed incomes are obviously the hardest hit by inflation. Rapid inflation is even worse because it creates price instability and uncertainty. Think, for a particularly extreme example, of Weimar Germany with the semi-apocryphal stories of people pushing wheelbarrows full of devalued German Marks to buy loaves of bread.

The Fed’s major tool for clamping down on inflation is to restrict the money supply, which means making the price of borrowing money from the Fed expensive. Up goes the prime rate. In the past 20 years, prime rates have moved on the order of .25 to .5 points per Fed meeting. Expect the Fed to engage in rapid adjustments of 1.5 to 2.5 percentage points per meeting.

Very quickly the lending rate will move from 4.75 (which is what Wells Fargo is offering today for a 30 year fixed) to 7, 9, 12, 15, 20. I think it’s heading north of 20 within 36 months. That is historically high, but in 1979/80, for a brief period, the interest rate was over 20 percent. People my parents age can remember home mortgages that cost 14 percent in 1979 or so. Expect much higher this time around as this economic downturn is a genuine crisis.

The high interest rates will make borrowing unaffordable for homeowners and businesses who want to do capital expansion. Housing prices will stay low with weak demand in the face of high mortgage rates. Economic growth will stagnate as businesses fail to create new jobs owing to the high cost of credit. More people will lose jobs, more defaults, more uncertainty.

In addition, there is a second housing bubble waiting to burst in 2010 and 2011 stemming from credit worthy borrowers who are in ARMs but who will have trouble refinancing because they have very little equity or negative equity in their homes and from non-credit worthy borrowers who have gotten loan workouts that are going to fail because they just don’t have the money to pay the mortgage. Greg recently wrote that 60 percent of the loan workouts done in the Spring 2008 have ended up in default already.

This second financial crisis will not just affect the people who made bad choices. It will affect a lot of people who were otherwise operating as if we were living in a normal economy the last five years.

The period of rapid inflation coming in the next year or two, followed by rapid interest rate hikes, will be catastrophic to people like my parents. For instance, someone on a $80,000 a year pension – many public service workers – have by today’s standards a pretty comfortable life style. But imagine just two years of 10 percent inflation, a not unreasonable rate given what happened in the late seventies. Two years of 10 percent inflation – 20 percent in aggregate – erodes the value of a $80,000/year pension (assuming no cost-of-living-adjustment) to the equivalent of about $64,000. That loss in value is unrecoverable, because the Fed never permits genuine deflation.

Consequently, retirees will be living on the equivalent of something like $64,000 a year, still not bad. But recall that normal inflation that’s considered normal/low over 10 years is still at 4 percent annually. That makes $64,000 the equivalent of $30,000 in fairly short order. Prudent investments now to simply maintain the value of money are difficult, so the key will be to reduce expenses and exposure that in 10 years, a retiree’s expenses are low enough that that person can get by on $30,000.

People on public pensions are in better position than most assuming they also have some money in a 401k. But you can imagine how people can go from very decent lifestyles, to ones that are not so awesome. Add to that the looming crisis in Social Security and Medicare. The tax rates to simply keep those programs afloat are going to be dramatically high.

The problem is sort of compounded in this sense by the fact that we got few of the benefits of socialism (say what you will about Sweden, but on a lot of measures for various reasons, the people there are fairly content), but by socializing the very wealthiest in society by bailing out the financial industry, and automakers, we are going to have all the costs of socialism.

The United States is not going to claim a unique position in 15 years of being the powerhouse economy. Now, to the extent that the United States can claim not to be Argentina, that will be because of two things: first, we have much more built up wealth thanks to the preceding 150 years, and second, the rest of the world may suffer worse.

But the fact of the matter is that in 1900, Argentina was the wealthiest country in the western hemisphere. It went from that point, to being eclipsed by the United States within 40 years because of the kind of economic policies that have kept Argentina much poorer (and which the United States has been engaged in for the past 15 years that have led to this crisis).

There are two possible, and linked benefits of this economic depression: the United States will no longer have the economic power to operate as the world’s policeman. Now, it’s entirely possible that, in the slide, the United States starts to use its residual military power as a way to extract from perceived enemies economic rents. Imagine threatening the Chinese over some semi-real or perceived dispute in order to get promises from the Chinese government to buy more of our debt or subsidize more imports into the U.S. That would be bad.

But it’s possible that, like the British, we start to unwind our commitments (which will involve some bloodshed as happened to the British in places like Rhodesia/Zimbabwe and so forth in the 1950s and 60s.)

The second benefit is that as our country ages, the government recognizes the value of immigrants in coming to the country (as has happened in Germany) to pay for the cost of the retired baby boomers, many of whom have not in fact earned their retirement. Now immigration has a downside. First, for racial and ethnic reasons, many Americans don’t like Hispanics. That’s unfortunate as Hispanics have powered segments of our economy without a lot of the legal or economic benefits going to them. Those benefits have been extracted by the middle class who have had them build their homes at low cost, and then turned around and complained complained about “illegals”.

The good news is that it could be marginally better than I describe.

The bad news is that it could be much, much worse.

Brian Brady says:

I read this on The Libertarians, yesterday. Joe’s thoughts are not rosy.

What if we selectively defaulted on the debt to China, as a response to the economic warfare they’ve waged upon us?

December 20, 2008 — 8:52 pm

Tom Vanderwell says:

Joe,

As Brian said, your thoughts are not rosy, but they are very logical and well thought out and very clearly echo the thoughts that have been bouncing around my brain as well.

Question for you (which has also been bouncing around my brain as well), for the real estate professionals and lenders who read here, what advice would you have for preparing for the oncoming problems?

I’ve got my own ideas, but I’d like to hear yours. Thanks!

Tom

December 20, 2008 — 9:21 pm

Michael Cook says:

I do have a couple of questions as well…

First, in this scenario, shouldn’t real estate prices spike in the near term as lending increases substantially? If this plays out as scripted by Joe, real estate fortunes could be made in the next five years. Typically, real estate has been a great place to be when inflation has run rampant.

Second, I think this is quite one sided. Globally, most economies are doing the same thing the US is doing on a smaller scale, given their smaller economy. Additionally, the US and China are far more linked than I think this article gives them credit for. Without our consumptions and exportation of manufacturing jobs to China and other recently developing nation, they would face serious economic destabalization. Combine that with troubles in the EU and Russia and I dont think its as simple as the US falling from grace so quickly.

This monetary scenario makes sense and could certainly be one of several that plays out in the next 10-20 years. I just question the conclusion. If everyone else is doing exactly what we are doing, how do we suppose they will be better off? China’s bailout, Japan’s bailout, the EU’s bailout and Russia’s bailout have all been large and have been equally inflationary. What will happen in their economies?

December 21, 2008 — 8:47 am

Joe Strummer says:

Mostly I wrote it not to say the exact predictions are going to pan out, but that we are fundamentally moving into a different era of American history, one in which the assumptions of the past 50 years about standards of living are not necessarily going to pan out.

Tom: I don’t have specific advice like, hedge your money here. If I had that kind of advice, I would be a money manager.

For the real estate agents, I have been impressed by Greg’s approach. (n.b.: Greg was my realtor when I was in Phoenix.) Be choosy about who acquire as clients, and be good at what you do. People will still need to buy and sell houses.

I also think creative financing options of the sort Greg laid out in his Arizona Republic column need to be re-learned, because just like the lay-away was the way to buy expensive items in the 1950s and 1960s, those sorts of purchasing options will probably return as the credit markets tighten for a sustained period of time.

I don’t know really anything about the lending business to say other than there are probably some analogies to pull from the way it operated back when rates were above 10 percent.

December 21, 2008 — 8:54 am

Joe Strummer says:

Real estate values would simply go up as the price level goes up. That doesn’t make anyone better off because the price of most things will simply rise with inflation.

Also, demand for real estate will suffer as interest rates rise to clamp down on inflation.

As I said, the US’ best hope is that all economies fall equally as hard. Or some do worse. Maybe this will happen. I think the days of American exceptionalism, if they ever existed, are over though.

We are not special.

December 21, 2008 — 9:48 am

J Boyer Morristown NJ says:

Ouch, I don’t like your predictions Joe. Can we all have a strong drink and start over? I guess lets hope the rest of the world takes at least the same hit we are taking. Not a nice thought though.

December 21, 2008 — 7:56 pm

Joe Strummer says:

Brian, as to your question about selective defaulting on the Chinese. First, I question the premise that the Chinese government has waged economic warfare on the people of the United States. I mean, the United States government is in the midst of bailing out specific industries, which is arguably a violation of various GATT/WTO provisions. That’s economic warfare of a sort. Besides, subsidization of Chinese industry just makes the goods cheaper to U.S. consumers (even though it may make it hard for U.S.-based companies to compete).

Second, I suppose one could selectively default, but these are multi-iteration games. And the Chinese government might decide that the U.S. is not a credible debtor, and not fund the U.S. government’s debt.

Notice, though, that I’m talking about the Chinese government and the U.S. government and consumers.

Really, it would be good to get beyond the whole mercantilist notion of trade deficits, but that’s for another blog and another day.

December 22, 2008 — 11:13 am

Sean Purcell says:

I think the days of American exceptionalism, if they ever existed, are over though.

We are not special.

In a world where no one is perfect, we are more perfect than most. This may explain some of your outlook.

December 23, 2008 — 2:56 pm

Brian Brady says:

“First, I question the premise that the Chinese government has waged economic warfare on the people of the United States.”

Happy holidays and thanks for the reply, Joe. I’m specifically addressing the PRC’s serial piracy of software, video, and music. That’s ongoing and is theft of intellectual property.

I know little about the one-sided trade agreements other than the rhetoric bandied about on conservative sites.

Let’s assume the hypothesis that the PRC is waging economic war against us, for this scenario. Do you think that a selective default would harm the PRC or US more?

December 24, 2008 — 9:14 am

Joe Strummer says:

Setting aside your and my disagreement over whether China has engaged in economic warfare, selective defaulting would probably harm us more simply because it would ensure that in the future China wouldn’t borrow from a country that didn’t feel obligated to pay its debts.

December 24, 2008 — 12:42 pm