Handyman Mark Deermer and I have been planning for this for a while: We’re going to ride the Phoenix real estate market back up by fixing and flipping some of the (many, many) distressed homes we work with. We’ve fixed up quite a few homes for buy-and-hold investors, and this is the logical next step in our praxis.

As with buying rental homes, it’s a matter of property selection before anything else. The right home, in turn-key condition, will sell at a substantial premium over its distress-sale price. By buying the right MLS-listed and court-house-steps properties, we can net out significant returns after all expenses.

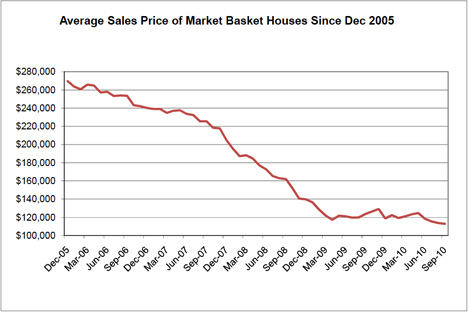

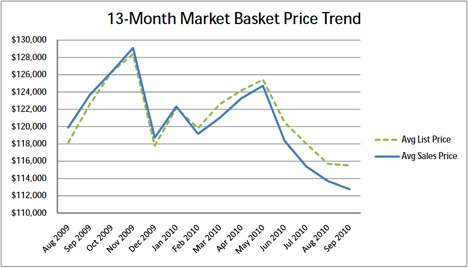

Buying right is everything, of course. If we overpay on the way in, we’ll have trouble extricating ourselves on the way out. We’re doing this now because the market in Greater Phoenix has reached a point where the math works fairly consistently. Houses that will flip profitably are still not common, but we’re to the point where they’re one among hundreds, rather than one among thousands.

The second step in the process is handling the refurbishing wisely and well — and quickly. Our goal is to get our properties back on the market within four days of taking possession of them. And we won’t be doing wish-and-a-promise fix-ups. Every house we do will have all new interior paint, all new flooring, all new window treatments and all new kitchen appliances. We want to give our buyers that model-home feeling — because they’ll pay more for homes that are white-glove clean and move-in ready.

And the third step is marketing, a process we get better at with every passing day. The homes we’ll be flipping will be completely refurbished, but they will also be staged for sale, with the kind of tasteful decorator touches that make people feel at home. We’ll build a marketing web site for each home, showing off what we’ve done with before and after pictures, and documenting the remodeling — both to defend the sales price and to assist the appraiser in seeing our justification for the sales price.

We’ll be pricing aggressively to the market, as well, thus to turn the money over more quickly. Our goal is to go from sold to sold in two months or less — with each investor’s money turning over six or more times a year.

Do you have stars in your eyes? The profit per home will not be huge. But because the money is turning over so rapidly, the annualized return-on-investment could be very substantial.

Why am I writing this? Because we need money to make this work. I’m going to be the marketing partner in the partnerships we’re putting together. Mark is going to be the work partner. What we need are finance partners.

The kind of houses we’re going to be working with are going to require around $100,000 in capital each. That will pay the acquisition costs plus the cost of refurbishing the home. Everything else — closing costs and unpaid liens — can be paid out of the resale proceeds at Close of Escrow. But each Limited Liability Corporation we put together is going to want $100,000 in seed capital. This can come from one or more finance partners, and the seed capital will be restored to the LLC after each house is sold, before any profits are disbursed.

Here’s the way to figure this: Even if the investor’s ROI is only 5% per flip, if we can turn that money over six times in a year, that’s a 30% annualized return. That’s good money by anyone’s standards — and the returns only stand to improve when the Phoenix real estate market finally gets back to an upward trajectory.

But what about down markets? God help us, it could happen. But this is why we’re working to sell the properties so quickly — and at aggressive prices — to get our money in and out before we can lose too much to declining values.

I’m not blowing smoke up anyone’s nose. We’ve been working on this problem for a year-and-a-half, all to make the numbers work. I’ll be documenting out projects here, so you can see what we’re up to.

Meanwhile, if you want to get in on this opportunity, speak up. We’re going to put together up to twenty of these partnerships, flipping as many as ten homes a month. This is a lot more aggressive than buy-and-hold investing — and a lot more risky, of course. But we’re offering the potential for truly astounding annualized returns. If you want to get involved in real estate on the supply side, here’s your chance.