Cited by BusinessWeek Online, a very eye-opening analysis of the sub-prime mess from National Review Online:

I’ve thought a lot about Rain Man over the past few months as I’ve been following the press coverage of the sub-prime mortgage crisis. The story’s been on the front page of the Wall Street Journal nearly every day. Pretty much every show on CNBC — except Kudlow & Co. and one or two others — has been obsessed with the topic. Yet no one seems to be asking the Rain Man question: “How big is the sub-prime mortgage market?”

And the answer, as Ben Stein makes clear, is not very big at all.

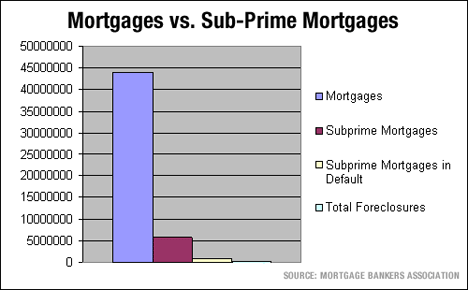

Currently there are about 44 million mortgages in the U.S., and less than 14 percent of them are sub-prime. And only about 13 percent of those are late on payments, with the majority of late payers working through their problems with the banks.

So, all in all, when you work through the details and get down to the number that really matters, only about 0.6 percent of U.S. mortgages are currently in foreclosure. That’s up a hair from roughly 0.5 percent last year. That’s it.

Actually, that’s not it. Things are actually better than the numbers suggest, since sub-prime-mortgage homes are less expensive than prime-mortgage homes. This makes sense. Wealthier people, generally, can afford costlier homes than less-wealthy people. The recent sub-prime surge brought large numbers of moderate-income families into the home-ownership market, and their houses are less expensive than most. Therefore, the dollar impact of the sub-prime default is smaller than if it were a prime default.

With approximately 254,000 mortgages in foreclosure at the moment — up from roughly 219,000 last year — the sub-prime meltdown has given us an increase of 35,000 mortgage foreclosures over the last quarter. Since the average sub-prime mortgage clocks in at almost exactly $200,000, we’re looking at an approximate $7 billion increase in foreclosed value in the first quarter of this year.

Raymond, how big is household net worth in the U.S.? About a hundred dollars?

Actually, it’s a lot bigger than that — about $53 trillion. In other words, the Read more