As you will have seen from yesterday’s short-list of entries, we had a lot of very high-quality posts among our contestants. This seems to augur well for the future of the contest. If you didn’t make the cut, soldier on. For the most part, even the posts that didn’t make it to the People’s Choice competition were very, very good.

As you will have seen from yesterday’s short-list of entries, we had a lot of very high-quality posts among our contestants. This seems to augur well for the future of the contest. If you didn’t make the cut, soldier on. For the most part, even the posts that didn’t make it to the People’s Choice competition were very, very good.

But: It’s plausible to me that you’re reading this post to hear about winners, so let’s talk about those:

The People’s Choice Award, the winner of the popular voting yesterday afternoon and evening and this morning, goes to Michael Cook, with Realtors, Wake Up and Start Helping Consumers.

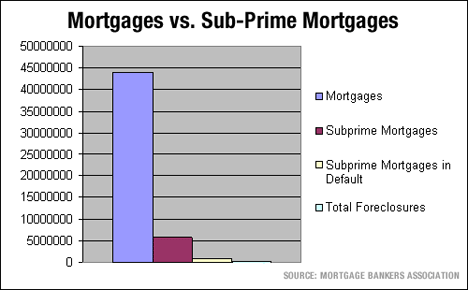

The Black Pearl is awarded to the entry that presents the best practical, technical or marketing idea of the week. This week that award goes to Benn Rosales for Mortgage drama, real estate bubble, tech crash, dotcom disaster. Here’s the winning idea:

The Black Pearl is awarded to the entry that presents the best practical, technical or marketing idea of the week. This week that award goes to Benn Rosales for Mortgage drama, real estate bubble, tech crash, dotcom disaster. Here’s the winning idea:

So now that we know it’s coming, what shall we all do about it? I’m doing a few things like; creating a shortsale team to assist sellers, offering move-down programs to those who aren’t so much in a bad way-yet, talking about it with sellers that call, offering advise on when to get out, and when to stay, talking to lenders about refinance options for those who might not need to move if we can do something now before they begin missing payments (not charging for that by the way, just guiding), calling past clients to see how they are, and that they’re okay.

And the first Odysseus Medal in this new competition, the overall best post of the week in my opinion, goes to Kevin Boer with The Innovator’s Dilemma In Real Estate: Beware Of That Redfin Swimming Just Below You. I’m a Grand Opera kind of writer, and Kevin is a just-the-facts kind of guy, but the journey he took us on in this post is simply extraordinary.

And the first Odysseus Medal in this new competition, the overall best post of the week in my opinion, goes to Kevin Boer with The Innovator’s Dilemma In Real Estate: Beware Of That Redfin Swimming Just Below You. I’m a Grand Opera kind of writer, and Kevin is a just-the-facts kind of guy, but the journey he took us on in this post is simply extraordinary.

I’ll be making the three ‘badges’ shown here available to the winners as ornaments to be used with their winning posts or on their sidebars. (And if a real artist wants to volunteer to make better versions, Read more